The Fed: Powell's Final Act. And It Was Anything But Quiet

A hold everyone expected. A split that nobody did.

The Decision

The FOMC voted to hold the benchmark federal funds rate at 3.50% to 3.75%, the third consecutive pause, in what may have been Jerome Powell's final meeting as chair. The hold itself was never in doubt. Markets had priced a 100% probability of no change. What caught attention was everything else.

The vote came in at 8 to 4, the most dissent the FOMC has seen since October 1992. Three of the four dissenters did not object to the hold itself, but to language in the committee's statement implying that the next rate move was likely to be a cut. They want the easing bias removed. In plain terms: a meaningful bloc of the committee believes the Fed is still leaning too dovish given where inflation sits.

Powell Stays

In a notable postscript, Powell confirmed he will remain on the Board of Governors after his chairmanship ends, waiting until the investigation into the Fed's building renovations is resolved with finality. The practical implication: there will be no open seat for Trump's ultra-dovish temporary appointee Stephen Miran when Kevin Warsh takes the chair. The committee will, for a period, skew more hawkish than it otherwise would have.

The Macro Backdrop

The Fed's restraint is rational given the data. Oil above $100 is feeding through into headline inflation. Services inflation excluding energy and housing has remained stubbornly above 3%. The labour market added 178,000 jobs in March with unemployment ticking down to 4.3%, not the profile of an economy that needs rate relief. The FOMC's statement acknowledged that the Middle East conflict is contributing to a high level of uncertainty, with inflation elevated due to the significant rise in global energy prices.

The tension the committee is navigating is real. Textbook monetary policy says to look through supply-driven inflation. But the longer Hormuz stays disrupted, the harder that becomes to justify, and if long-term inflation expectations start drifting meaningfully higher, the calculus flips from "hold" to "consider tightening."

Oil: The Market Priced in Resolution. Reality Had Other Plans.

Brent at $126. Hormuz still blocked. Asia taking the most pain.

Oil surged past $125 this week, its highest level since the conflict began, after Trump confirmed the Strait of Hormuz blockade would continue until Iran agreed to a deal on its nuclear programme. Reports also emerged of US military commanders briefing the president on a plan for a "short and powerful" wave of strikes, adding a new escalation layer the market had not fully priced.

"The oil market has moved from over-optimism to the reality of the supply disruption we are seeing in the Gulf." - ING analysts

The geographic asymmetry of the damage is sharp. Asian markets absorbed the most selling pressure, with Japan the taking the brunt of it. The Topix fell 1.5%, 30-year JGB yields rose to 3.7%, and the yen briefly touched ¥160.47, approaching levels where authorities have previously intervened. India's 10-year yield hit 6.99% while the rupee weakened to a record low against the dollar. Countries across South and Southeast Asia with limited fiscal buffers and lower energy reserves are facing the most direct pressure on government borrowing costs.

US equity futures, by contrast, rose modestly on the day. The Nasdaq was up 0.4%. The divergence is stark, and it reflects a structural reality that continues to define this crisis. The US, as a net energy exporter, is insulated in a way Asia simply is not.

Big Tech Earnings: The Numbers Were Stellar. The Market Asked What Comes Next.

$725 billion in combined AI capex. 60% collective earnings growth. And the stock that fell the most was the one whose story was hardest to follow.

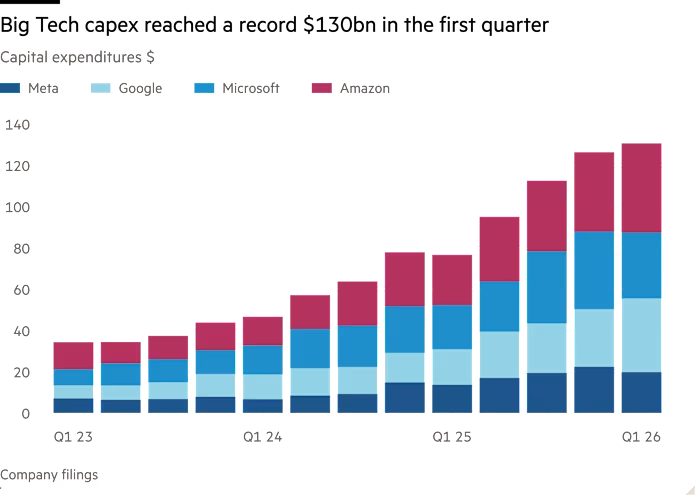

The big four hyperscalers, Amazon, Microsoft, Meta, and Alphabet, reported collectively strong results, with combined earnings growth of 60% year-on-year and revenue growing at roughly 20% across the group. Together, they are now projecting $725 billion in capital expenditure this year, up 77% from a record $410bn in 2025. The AI buildout is not slowing, it is accelerating.

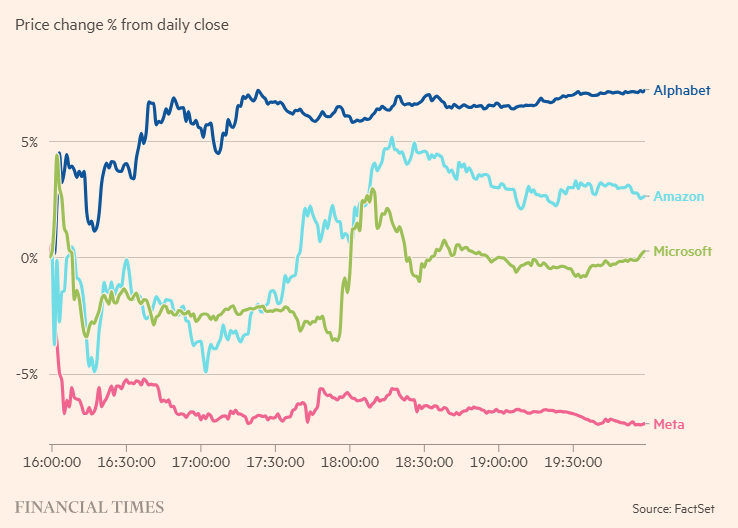

But the market did not treat all four equally.

Why Alphabet won the week

Google Cloud revenue grew 63%, and Alphabet now holds a $460 billion backlog of data centre contracts. AI-enhanced search drove ad revenue up 19%. The spend connects directly to a product that is already working. Investors can model it. Alphabet's market cap is on track to open Thursday at a record $4.3 trillion.

Why Meta didn't

Meta's revenue jumped 33%, a number most companies would celebrate. But the market focused on what it couldn't see: a credible AI product roadmap. Muse Spark is not considered cutting edge. Zuckerberg said he cared more about quality than hitting a deadline on new model releases. Combined with a $10 billion capex increase and rising memory costs, the market responded by wiping roughly $113 billion in market cap in after-hours trading.

"Investors are not interested in growth at any cost." - Dec Mullarkey, SLC Management

The distinction between Alphabet and Meta this week is the same distinction that will define this entire earnings cycle: it is not how much you spend, it is whether the spend has a visible, credible connection to revenue.

Japan Draws a Line in the Sand: Yen Intervention and the Golden Week Warning

A suspected intervention. A two-year low. And a finance ministry warning that more is coming.

The yen lurched violently on Thursday, plunging to ¥160.70 before surging more than 2.5% to ¥155.50 within hours, in what a Japanese government official confirmed was a direct currency intervention. By Friday, the yen had already begun slipping back to around ¥157.20, and Japan's top currency diplomat Atsushi Mimura issued a pointed warning to speculators: the authorities are watching, and they are prepared to act again.

The timing is deliberate. Golden Week, Japan's extended national holiday running from Saturday through Wednesday, thins out trading volumes significantly, amplifying the market impact of any government purchases.

"Golden week is a very good time to intervene, lower volumes mean the intervention achieves more. You get much more bang for your buck." - Stefan Angrick, Moody's Analytics

Why the Yen Is Under Pressure

Japan's sensitivity to yen weakness has intensified since the outbreak of the Middle East conflict. The country is heavily dependent on imported energy, food, and raw materials, and a weaker yen directly amplifies the cost of every barrel of oil it buys, feeding into the inflationary pressure the BOJ is already struggling to contain.

The structural drag is compounding the problem. The yen continues to function as a global carry trade funding currency. Investors borrow cheaply in yen to fund positions in higher-yielding assets elsewhere, creating persistent downward pressure that is largely disconnected from Japanese economic fundamentals. Even as the BOJ gradually raises rates and narrows the yield spread between Japanese and US government bonds, the yen has not responded as theory would suggest.

What the Intervention Signals

The last time Japan intervened in currency markets was in 2024, also around the ¥160 level, deploying approximately $100bn across a series of moves. The fact that the yen has returned to the same threshold and required intervention again, illustrates the limits of what the BOJ can achieve through rate normalisation alone when the macro backdrop is this unfavourable.

Mimura indicated that Japanese authorities are in constant contact with their US counterparts, suggesting the intervention carried Washington's tacit blessing and would not strain the alliance. That matters: unilateral currency intervention without US support has historically been less effective and more politically costly.

The Bigger Picture

The yen situation crystallises a tension that has been building since the conflict began. Prime Minister Takaichi won her February election on a platform of protecting Japanese households from rising prices, a promise that becomes harder to keep the longer the yen stays weak and Brent stays above $100. The BOJ issued a rare warning Thursday that inflation could "deviate considerably" from its baseline forecasts. That language, coming alongside a rate hold, reflects the bind the central bank is in: raising rates more aggressively to defend the yen risks choking a fragile recovery; staying on hold risks a stagflationary spiral driven by imported inflation.

Golden Week provides a tactical window. Whether the authorities can build lasting upward momentum in the yen, rather than just interrupting a downtrend, is the question that will define the next chapter of Japan's macro story.

View Forward

The results this week broadly validated the AI investment thesis. Cloud growth is real. AI revenue is converting. The hyperscalers are not burning capital into a void. That matters for market confidence going into the second half.

But three things are worth sitting with.

Positioning is getting aggressive. Morgan Stanley's Senior Portfolio Manager Andrew Slimmon flags that US equities look stretched after a near 10% rally, with strong earnings now largely priced in. A short-term pullback is likely and, in his view, healthy, a reset of positioning rather than a structural reversal. The longer-term earnings cycle, particularly in banks, remains supportive of the broader uptrend.

The oil risk has not been resolved, it has been deferred. Markets have shown they can tolerate $100 oil. The question is $120, sustained. At current levels, the energy shock is beginning to feed through into Asian sovereign spreads and yen pressure in ways that did not exist a month ago. If the Hormuz blockade extends into the summer, the macro picture in Asia deteriorates faster than current equity pricing implies.

The Fed transition is a genuine variable. Warsh inherits a committee with four dissenters, an incoming leadership resisting the easing bias, services inflation above target, and a president demanding lower rates. How he navigates the first June meeting, whether he signals continuity or a shift in posture, will set the tone for rate expectations through year-end. Powell staying on as governor is a stabilising force, but it does not resolve the underlying tension between the hawks on the committee and the political pressure from above.

The base case remains constructive: solid earnings, AI capital cycle intact, no imminent recession signal. But the rally has been fast, positioning has followed it, and the two variables that could interrupt it, oil escalation and a hawkish Fed signal, are both live. This is not a moment to be adding risk aggressively. It is a moment to observe.

Weekly Market Snapshot

Indices

SPX: +0.91%

NDX: +1.49%

SOX: +0.78%

VIX: -9.19%

Treasuries

US 2Y: +2.62%

US 10Y: +1.58%

FX

USD/JPY: -1.42%

USD/CNH: -0.07%

Commodities

Brent: +2.79%

XAU/USD: -1.95%

On the Radar

Date | |

|---|---|

Monday 04/05 |

|

Tuesday 05/05 |

|

Wednesday 06/05 |

|

Thursday 07/05 |

|

Friday 08/05 |

|